Understanding FEOC: What Clean Energy Developers Need to Know as Compliance Becomes Market Standard

SHARE

PUBLISHED

Mar 6, 2026

AUTHOR

Erik Underwood,

CEO & Co-Founder of Basis Climate

MEDIA CONTACTS

Foreign Entity of Concern (FEOC) compliance has moved faster than most clean energy developers expected. What initially appeared as a policy initiative tied to national security has quietly become a factor that shapes real project outcomes—eligibility for tax credits, financing timelines, and how confidently a project can be taken to market.

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, introduced sweeping FEOC restrictions that fundamentally reshape eligibility for clean energy tax credits. On February 12, 2026, the IRS released Notice 2026-15, providing the first detailed interim guidance on how to calculate whether projects and manufactured products comply with the new rules.

These rules are designed to curtail reliance on supply chains connected to China, Russia, North Korea, andIran. For tax credit buyers and sellers in the transfer market, FEOC compliance has become a critical diligence item that directly affects credit eligibility, pricing, and transaction risk.

At Basis, we see FEOC not as an abstract compliance exercise, but as part of a necessary shift in how clean energy projects are assessed and tax credits monetized. As FEOC compliance becomes a market standard, understanding FEOC—early and clearly—is becoming essential.

Key Takeaway for Buyers

FEOC restrictions apply to technology-neutral credits (Sections 45Y, 48E) and manufacturing credits (Section 45X). Legacy credits claimed under Sections 45 and 48 on projects under construction by the end of 2024 are not affected, while 45X credits through 12/31/2025 are generally not affected. Buyers should prioritize understanding whether credits they purchase are subject to FEOC and factor compliance costs into pricing.

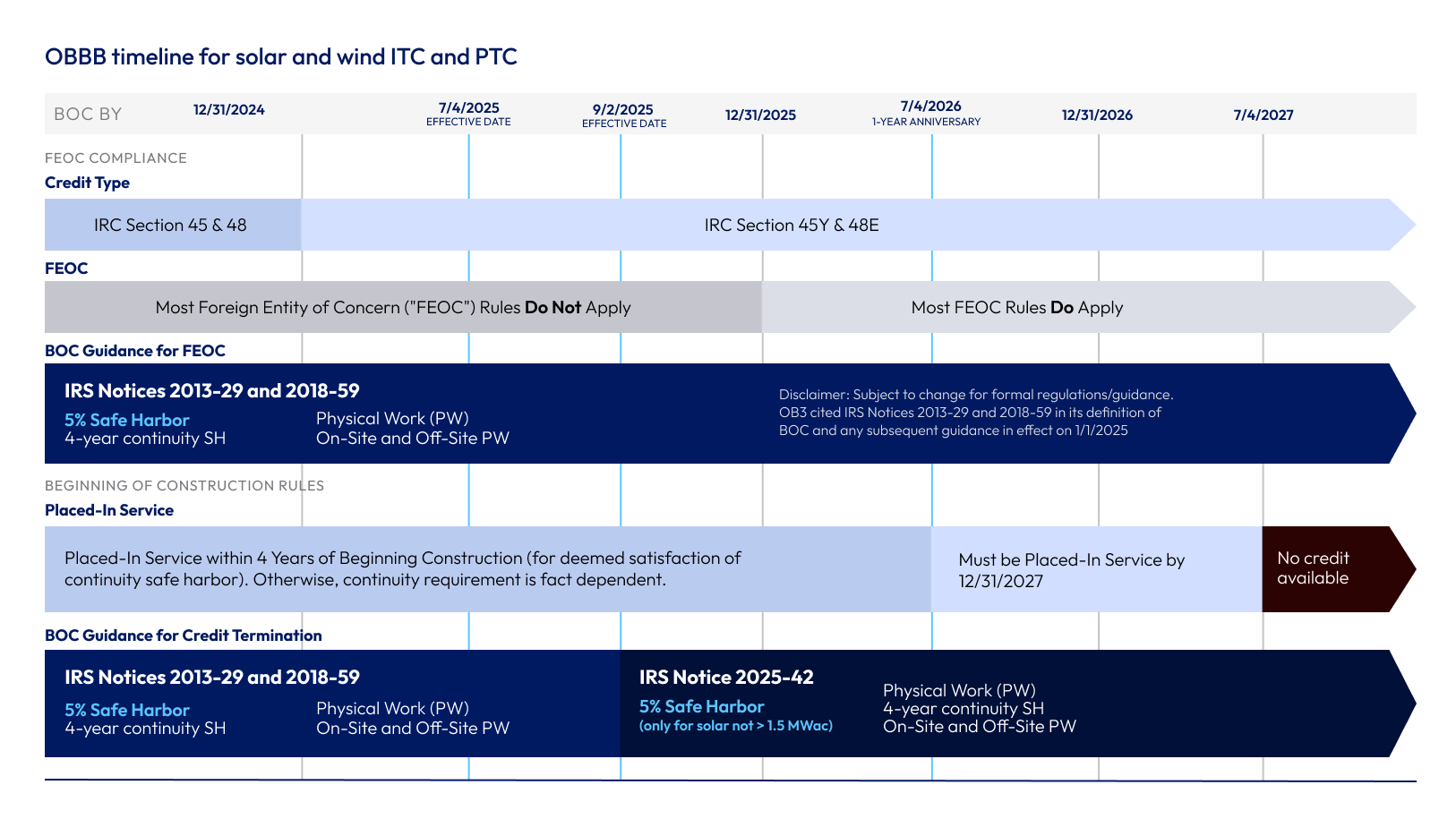

Timeline for FEOC Safe Harboring

Below is the timeline for projects to be safe-harbored into prior beginning of construction (BOC) dates, how long they have until placed-in-service, and whether they are under FEOC compliance requirements.

The Guidance Is Out

February's guidance (Notice 2026-15) provided one of the clearest signals yet. Teams are reviewing ownership structures, revisiting contracts, and beginning to map supply chains—often well before regulators provide full clarity. Tax credit buyers, investors, and intermediaries are already asking questions about FEOC exposure, and projects that can't answer them cleanly tend to slow down.

In practice, FEOC is starting to function like other familiar diligence areas. At first, it feels ambiguous.Then it becomes standard table stakes. We're now somewhere in the middle of that transition.

Which Tax Credits Are Affected?

The FEOC restrictions apply to three categories of federal clean energy tax credits:

Section

Description

45Y

Clean Electricity Production Credit (technology-neutral PTC)

Critically, legacy tax credits under Sections 45 and 48 are exempt from these rules. Projects that were under construction for tax purposes by the end of 2024 can claim legacy credits without FEOC compliance. This exemption has made legacy credits highly sought-after in the transfer market, and they are expected to trade at a premium as supply diminishes.

The OBBBA also prohibits the transfer of any tax credits under Sections 45Q, 45U, 45X, 45Y, 45Z, or 48E to specified foreign entities under Section 6418.

The Three-Step FEOC Analysis

The FEOC rules distill into at three-step framework that applies separately to power/storage projects and to manufacturers claiming 45X credits. Each step must be satisfied independently.

Step 1: Material Assistance from Prohibited Foreign Entities

The first restriction limits the amount of equipment, parts, and materials supplied by prohibited foreign entities (PFEs) that can be incorporated into projects or products on which tax credits are claimed. This is the area addressed by Notice 2026-15.

The Material Assistance Cost Ratio (MACR) is the centerpiece metric. It measures the proportion of non-PFE costs in a project or product:

MACR Formula

MACR = (A – B) ÷ A

A = total direct cost of manufactured products/materials. For 45Y/48E, this is the taxpayer's acquisition cost of manufactured products incorporated into the facility (project owners do not need to reconstruct the manufacturer's internal cost structure). For 45X, this is the manufacturer's direct material costs only (excluding labor) for constituent materials.

B = cost of items supplied by PFEs.

The MACR must meet or exceed minimum thresholds that vary by technology type and year. The thresholds increase over time, requiring progressively higher proportions of non-PFE sourcing.

MACR Thresholds for Power Projects (Sections 45Y/48E)

Construction Start

Qualified Facilities

Energy Storage

2026

40%

55%

2027

45%

60%

2028

50%

65%

2029

55%

70%

2030+

60%

75%

MACR Thresholds for Manufacturing (Section 45X)

Year Sold

Solar

Wind

Battery

2026

50%

85%

60%

2027

55%

90%

65%

2028

65%

N/A*

70%

2029

75%

N/A*

75%

2030+

85%

N/A*

85%

* Section 45X credits cannot be claimed on wind equipment produced and sold after 2027.

Important limitation: The above thresholds and safe harbor pathways apply primarily to technologies with existing domestic content safe harbor tables (solar, wind, battery storage). Technologies without such tables—including nuclear, geothermal, fuel cells, fusion, and thermal storage—face significantly higher compliance burdens and cannot use the Identification or Cost Percentage Safe Harbors. They may still use the Certification Safe Harbor, but must await new PFE-specific safe harbor tables (due by December 31, 2026) for a streamlined pathway.

Key Provisions from Notice 2026-15

Topic

Explanation

Scope of calculations

Only the manufactured products (MPs) and manufactured product components (MPCs) identified in IRS safe harbor tables must be included in the MACR calculation. For solar projects, calculations begin at the cell level and include components such as frames and junction boxes.

Per-facility calculation

The MACR must be calculated separately for each “qualified facility,” such as each MV inverter circuit, wind turbine, or other portion of a project that can be placed in service independently.

Manufacturer averaging

Manufacturers may average their direct material costs over time periods of up to one year, which provides flexibility in calculating the ratio.

Interim safe harbors

Until new safe harbor tables are issued (due by December 31, 2026), taxpayers may rely on the domestic content tables from Notices 2023-38, 2024-41, and 2025-08. These tables apply to solar, onshore wind, offshore wind, and battery projects. Important: The MACR calculation mechanics differ from domestic content. For MACR, if a listed component is not incorporated into the facility, its assigned cost percentage is excluded from both numerator and denominator. For domestic content, unused listed components remain in the denominator at zero value. This distinction can materially affect results.

Exclusions

Steel and iron construction materials, along with main power transformers, may be excluded from the MACR calculation.

PFE determination timing

A supplier’s status as a Prohibited Foreign Entity (PFE) is generally determined on the last day of the supplier’s tax year in which the project owner or manufacturer paid for the equipment.

Supplier certificates

Taxpayers may rely on supplier certificates confirming the supplier is not a PFE under the Notice’s Certification Safe Harbor, provided they have no reason to know the certificate is inaccurate. If a taxpayer knows or has reason to know a certificate is inaccurate, all costs of the relevant MP, MPC, or constituent material must be treated as PFE costs.

Interconnection property

For Section 48E projects, a separate MACR calculation is required for qualified interconnection property (QIP). If QIP fails the MACR test, the facility can still qualify for credits but cannot include QIP expenditures in the qualified investment. However, if the facility itself fails MACR, no credit is available even if the QIP passes independently.

Freight and tariffs

Notice 2026-15 explicitly includes freight and tariff costs as direct costs in the MACR calculation. Given the current tariff environment, this can materially affect MACR outcomes and should be modeled during procurement planning.

Repowered projects

For repowered projects, the material assistance calculation only includes the new equipment added as part of the repowering.

Step 2: Taxpayer-Level FEOC Restrictions

The second restriction examines whether the entity claiming or selling tax credits is itself too closely tied to a foreign adversary. Entities classified as a "specified foreign entity"(SFE) or "foreign-influenced entity" (FIE) are barred from claiming technology-neutral credits in any year they hold such status.

SFESpecified foreign entity

An entity qualifies as an SFE if it meets any of the following conditions:

More than 50% owned by the government, citizens, or nationals of China, Russia, North Korea, or Iran (excluding US citizens, nationals, or green card holders)

More than 50% owned by entities organized or headquartered in one of those four countries

Specifically named entities such as CATL, Gotion, BYD, EVE Energy Company, and Hithium Energy Storage Technology

Companies listed on the OFAC sanctions list

Companies that benefit from Uyghur forced labor in Xinjiang

FIEForeign-influenced entity

The FIE test casts a wider net. A taxpayer is considered an FIE if any of the following apply:

An SFE has direct authority to appoint a board member or an executive-level officer (president, CEO, COO, CFO, general counsel, or senior VP)

A single SFE owns 25% or more of the taxpayer

Two or more SFEs collectively own 40% or more

SFEs hold 15% or more of the taxpayer’s outstanding debt (measured at original issuance)

The OBBBA changed this standard from “held by” to “issued to” SFEs, creating significant ambiguity for publicly traded debt instruments. This definitional question remains unresolved in Notice 2026-15.

Tested:Status is assessed annually on the last day of each tax year.

Status is tested annually on the last day of each tax year. Many publicly traded companies and their 80%-or-more-owned subsidiaries are shielded from these restrictions, though they can still be caught by the contract payment rules in Step 3 or if an SFE has authority to appoint a board member or executive officer.

Ownership is usually the first place developers start when assessing FEOC risk, but the analysis goes well beyond headline equity percentages. Governance rights, board seats, and voting power all matter. Even relatively small ownership positions can raise questions if they come with outsized influence over decision-making. Parent entities, joint venture partners, and affiliated companies involved in generating or monetizing tax credits may all be relevant.

Step 3: Effective Control Through Contracts

The third restriction targets contracts and technology licenses with SFE counterparties that give the SFE"effective control" over the taxpayer, project, or product. Any payments under such contracts will make the taxpayer a "foreign-influenced entity" with respect to the relevant project.

If there's one area where FEOC compliance is most challenging, it's contracts. Even where ownership and governance are clean, certain contractual arrangements can create what regulators describe as "effective control." This can arise through technology licensing, software dependencies, long-term O&M agreements, or exclusive service arrangements tied to core project functions.

Contract Clauses to Avoid

Category

Contract Clauses Considered Evidence of Effective Control

Power / Storage Projects and Manufacturing Facilities

- Allowing the counterparty to determine the amount or timing of production or output

- Giving the counterparty rights to determine who can purchase the output or products

- Restricting access to critical production data to the counterparty or its agents

- Allowing the counterparty to maintain, repair, or operate equipment on an exclusive basis

- Allowing the counterparty to specify or direct sources of components, subcomponents, or critical minerals

- Giving the counterparty rights to direct the operation of the project or production facility

- Limiting the taxpayer's use of intellectual property related to the project or product

- Allowing royalty payments for more than 10 years

- Requiring the taxpayer to hire the counterparty for more than two years of services

CRITICAL: New Licenses After July 4, 2025

Any new licensing arrangement with a Specified Foreign Entity (SFE) signed on or after July 4, 2025 is automatically treated as giving the counterparty effective control. Modifying an existing IP license with an SFE after that date triggers the same presumption. The only exception is a bona fide purchase or sale of intellectual property where ownership does not revert to the counterparty.

Supply Chains and Material Assistance

FEOC considerations don't stop at entities and contracts. They extend into the physical components that makeup a project. For certain credits, developers must demonstrate that a sufficient portion of project costs is not attributable to prohibited foreign entities. That requirement introduces a material assistance analysis that depends on supply chain visibility, cost attribution, and documentation.

For many teams, this is unfamiliar territory. Mapping suppliers, requesting certifications, and tracing component origins are becoming part of standard development work. While methodologies are still evolving, expectations around traceability are already influencing procurement decisions.

Strategic Interaction with Safe Harbors

Notice 2026-15 provides a tiered approach to supplier certificates. You can rely on them for MACR calculations under the Notice's designated "Certification Safe Harbor," but this reliance is not unconditional—you cannot rely on a certificate if you know or have reason to know it is inaccurate.

The "Reason to Know" Standard

The most critical caveat is that reliance is permitted only if you have no "reason to know" the certificate is inaccurate. You cannot ignore red flags. If a supplier provides a certificate claiming no PFE content for a product type known to be exclusively manufactured in a covered nation, the IRS may deem your reliance unreasonable.In practice, this means performing a baseline level of supply chain reasonableness checks.

Mandatory Certificate Requirements

To be valid for MACR substantiation, each certificate must meet a strict checklist:

Must come from your direct supplier

Must be signed under penalties of perjury by an authorized officer of the supplier

Must include the supplier's Employer Identification Number (EIN)

Must explicitly state the property was not produced by a PFE and that the supplier does not know (or have reason to know) that any MPC in the chain of production was produced by a PFE. Note: attestation stops at the MPC level—suppliers do not need to trace beyond MPCs to subcomponents or raw materials.

Records must be retained for at least six years and a summary attached to your tax return

Compliance Pathway Comparison

Pathway

Certification Burden

Reliability

Direct Cost Method

High: Requires certifications for specific cost amounts from direct suppliers who must often vet sub-suppliers.

Most accurate, but highest audit risk if sub-suppliers fail.

Identification Safe Harbor

Medium: Use 2024–2025 Safe Harbor Tables to identify components. Only need to certify the source, not internal cost data.

Recommended for solar and wind projects using standard BOMs.

Cost Percentage Safe Harbor

Low: Rely on IRS-assigned percentages for each component category. Certifications only need to confirm non-PFE status.

Most bankable for financing, as it removes the need to share sensitive vendor cost data. Note for 45X: this method allows counting "Production" line items (analogous to labor costs), while the direct cost method excludes labor—meaning the same component can pass or fail MACR depending on methodology chosen.

Penalties and Enforcement

The OBBBA significantly increases the stakes for compliance errors:

Extended statute of limitations: The IRS has six years (rather than the usual three) to challenge material assistance calculations after a return is filed.

Taxpayer penalty: A 20% penalty applies if material assistance miscalculations result in more than 1% underpayment of tax. For corporations, the threshold is $10 million or 1%, whichever is less.

Supplier penalty: Suppliers providing false certificates face penalties of 10% of the resulting tax reduction claimed by the customer, subject to a minimum threshold. This applies to certificates given after December 31, 2025.

ITC recapture: For technology-neutral ITCs, the full credit must be repaid if the taxpayer makes payments under contracts giving an SFE effective control in any of the 10 years after the project is placed in service.

Date

Significance

June 16, 2025

Cutoff for binding purchase orders that can be excluded from MACR calculations.

July 4, 2025

OBBBA enacted. New IP licenses with SFEs after this date automatically trigger effective control. SFE/FIE restrictions apply to tax years beginning after this date.

Dec. 31, 2025

Projects under construction by this date can skip the material assistance calculation (Step 1). Supplier penalty rules take effect for certificates given after this date.

Jan. 1, 2026

FEOC restrictions take effect for calendar-year taxpayers. Material assistance rules apply to projects starting construction in 2026+.

Feb. 12, 2026

IRS releases Notice 2026-15 with interim guidance on MACR calculations.

Mar. 30, 2026

Deadline for public comments on Notice 2026-15.

July 4, 2026

Solar and wind projects must begin construction by this date (or be placed in service by Dec. 31, 2027) to qualify for technology-neutral credits.

Dec. 31, 2026

IRS deadline to publish new safe harbor tables for MACR calculations.

Implications for the Tax Credit Transfer Market

The introduction of FEOC rules is reshaping the clean energy tax credit transfer market. Projects with clear, well-documented FEOC profiles tend to move through transactions more efficiently, while projects with unresolved questions often experience delays, added scrutiny, or pricing pressure.

Legacy credit premium: Legacy Section 45 and 48 credits, which are exempt from FEOC, are trading at a premium and will continue to do so as supply diminishes.

Pricing pressure on tech-neutral credits: Credits subject to FEOC compliance are expected to experience lower pricing until investors develop comfort with the compliance framework.

Enhanced diligence requirements: MACR compliance has become a financing diligence item. Lenders, tax equity investors, and credit buyers all require audit-ready MACR documentation files, including supplier certifications, bills of materials, and country-of-origin attestations.

Supply chain shifts: Several Chinese-owned solar manufacturing facilities in the US are being sold to domestic operators, helping to de-risk supply chains but potentially introducing short-term disruptions.

45X market lag: Many 45X credit sellers have been focused on understanding FEOC compliance and have been less active in the transfer market, creating a temporary lag.

Guidance for Credit Buyers

Assess FEOC exposure early: Determine whether credits being purchased are subject to FEOC restrictions or fall under the legacy exemption.

Demand audit-ready documentation: Request MACR calculations, supplier certificates, and evidence of PFE status reviews from sellers.

Price FEOC risk appropriately: Factor increased compliance costs and the risk of credit disqualification into pricing for technology-neutral credits.

Monitor reliance windows and evolving guidance The IRS plans to release additional FEOC guidance on a rolling basis, including regulations on PFE definitions, effective control, and updated safe harbor tables. The interim MACR rules and safe harbors have a 60-day transition period after Treasury publishes proposed regulations or new safe harbor tables. Factor this timing into construction start decisions

Consider multi-year strip agreements: For 45X credits from sellers with straightforward FEOC compliance profiles, multi-year purchase commitments can provide pricing stability.

Guidance for Credit Sellers

Build MACR files proactively: Lock supplier representations into contracts and collect bills of materials and country-of-origin documentation as you procure.

Review all SFE relationships: Identify any contracts with SFE counterparties and scrub them of effective control provisions.

Obtain supplier certificates promptly: Retain certificates confirming suppliers are not PFEs for at least six years.

Consider PTC vs. ITC implications: The ITC recapture provision (full credit repayment for 10 years if SFE effective control is triggered) may make PTCs more attractive for some projects.

Financing in 2026? Don't Let FEOC Be Your Deal-Breaker

If you're planning to finance or break ground this year, your bankability depends on mastering the three work streams above. Documentation is your only defense. Between supplier certifications and MACR modeling, the "wait and see" approach is officially over.

THE BOTTOM LINE

The "wait and see" approach to FEOC is officially over. Between supplier certifications, MACR modeling, and contract reviews, preparation isn't optional—it's expected. Developers who address FEOC early will preserve project value and maintain access to capital.

Outstanding Guidance and Looking Ahead

Notice 2026-15 addresses only one leg of the three-step FEOC framework: the material assistance calculation.The IRS has indicated it will release further guidance on a rolling basis. Key areas still awaiting clarification include:

Detailed rules for determining PFE status, including complex multi-national ownership structures

Guidance on the "effective control" analysis and the 13 contract clause tests

Updated safe harbor tables (due by December 31, 2026)

Anti-circumvention rules

Comprehensive proposed regulations (not expected in the near term)

Regulatory guidance will continue to refine definitions, thresholds, and methodologies. But the broader direction is unlikely to change. Scrutiny around foreign influence in clean energy is here to stay, and FEOC is a central mechanism driving that scrutiny.

Final Thoughts

FEOC marks a meaningful shift in clean energy development. It reflects a closer alignment between policy, national security, and capital markets—one that is reshaping how projects a reevaluated and monetized. As compliance and documentation become market standard, developers who understand FEOC and engage with it early will be better equipped to protect project value and maintain access to capital.

.svg)

.svg)