.svg)

Insight

This update builds on our prior transferable tax credit pricing analysis and reflects where the market stands today

Jul 1, 2026

This update builds on our prior transferable tax credit pricing analysis and reflects where the market stands today

Today, the number of tax credit buyers in the transfer market continues to grow, but the seasonality of credits, diversification in credit preferences, and continued impact of the One Big Beautiful Bill Act (“OB3”), are all having varied downward impacts on tax credit pricing, especially for §48/48E ITC pricing. The clearest driver is simple imbalance. A wave of credits carried into and generated through the second half of 2025 met a buyer base that did not expand at the same pace.

Taken together, the 2025-vintage focus, FEOC concern and the rotation toward various PTCs should continue to push ITC pricing downward in the near term.

A 45X manufacturing ramp

Advanced-manufacturing production is scaling, and §45X credits scale with it. More domestic output means more credits, and that incremental supply is beginning to press on the lower end of §45X pricing even as the headline range holds. Many buyers are still seeking tax insurance on §45X credit.

Ethanol-driven 45Z volume

A large volume of §45Z clean-fuel credits — many tied to ethanol production — is now coming to market. That issuance adds real supply and is a contributor to the downward drift.

Residential platforms selling low for working capital

A new generation of residential clean-energy finance platforms is turning to the transfer market for working capital and seeking to sell on a monthly or quarterly basis. Not many ITC buyers are ready to transact with new entities, which means newcomers may choose to accept lower pricing in order to receive interest and receive cash payments earlier.

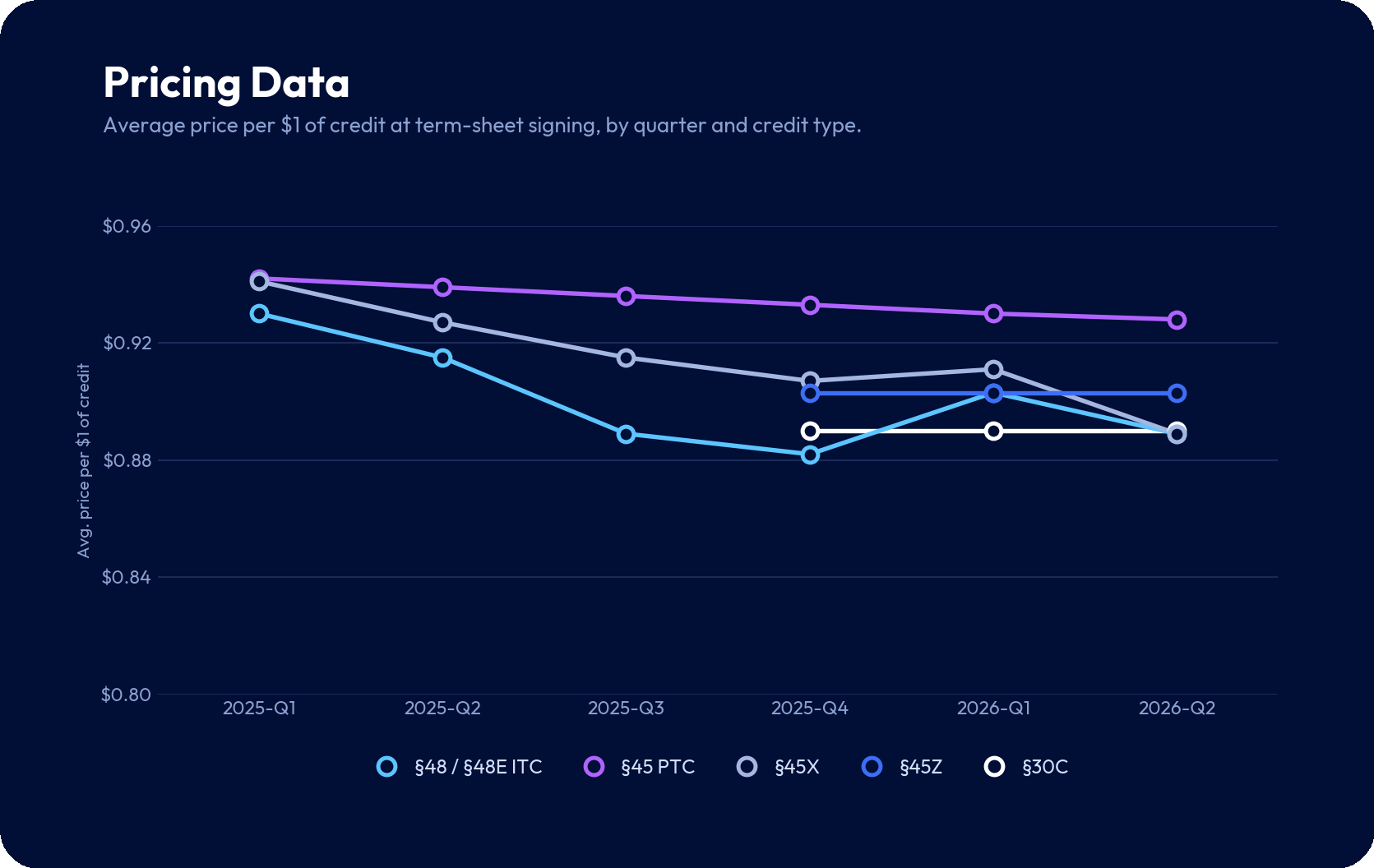

The trend is clearest when our executed transfers are averaged by the quarter in which the term sheet is signed. Production credits (§45 PTC) have held mostly firm, while ITC pricing decreased through the back half of 2025 and into 2026. §45X has held near the top of its range with a recent softening.

The ranges below are indicative of where Basis is currently observing market pricing today for transactions above $5m in credits. Any individual transaction prices to its own facts — credit type, size, insurance, indemnity package, prevailing-wage and adder status, and seller credit quality all move the number. Buyers continue to demand that credits are insured unless they come with a rock solid guarantee across credit types.

For sellers: this is a market that rewards being easy to transact. Clean documentation, a credible insurance and indemnity package, and a well-defined credit story matter more when buyers can be selective. Sellers of ITC should expect to compete on price and should weigh timing considerations against purchase price.

For buyers: the current imbalance is an opportunity to lock in attractive pricing for 2026 credits, with the widest spread on ITCs and emerging segments like §45Z / §45X where new supply from new sellers. We expect the supply-heavy tone to persist in the near term.

As always, the right price for any given credit is the one its specific facts support — and that is the conversation we have with clients on every transaction.

This is market commentary. It is not tax, legal, accounting, or investment advice, and it is not a published price index. Pricing on any transaction depends on its specific facts. For guidance on a particular credit or transaction, contact the Basis Climate team.