.svg)

Insight

Treasury and IRS released Notice 2025-31 on June 23, 2025, updating energy community eligibility lists that could significantly impact your clean energy project's tax credit bonuses.

Jul 14, 2025

Treasury and IRS released Notice 2025-31 on June 23, 2025, updating energy community eligibility lists that could significantly impact your clean energy project's tax credit bonuses.

On June 23, the Treasury Department and Internal Revenue Service issued Notice 2025-31, which includes updated lists for determining energy community eligibility under the Statistical Area Category and Coal Closure Category. For clean energy developers, this annual update can mean the difference between securing a 10% increase to a project's credit value or missing out on the bonus financial incentives.

The new guidance brings both opportunities and challenges. The energy community status listed in the notice is applicable as of June 23, 2025, and will continue until Treasury and the IRS issue an updated list based on unemployment rates for calendar year 2025.

Statistical Area Category Expansion

The most significant change in this year's update is the expansion of eligibility criteria. The notice expands eligibility under the Statistical Area Category by adding a parallel analysis using the revised statistical areas from the 2020 census, in addition to the existing 2010 census areas. This means projects located in counties that shifted statistical areas between the two census years may now qualify if either statistical area meets the applicable criteria.

The updated list uses 2024 calendar year county unemployment rates released on April 18, 2025, by the Local Area Unemployment Statistics program of the Bureau of Labor Statistics.

Coal Closure Category Updates

The Coal Closure Category has also received important updates. The notice provides two lists of census tracts relevant to the Coal Closure Category. One list identifies tracts added because of data corrections, which qualify retroactively, meaning projects placed in service in any of these tracts in 2023 or later are potentially eligible for the energy community bonus.

.svg)

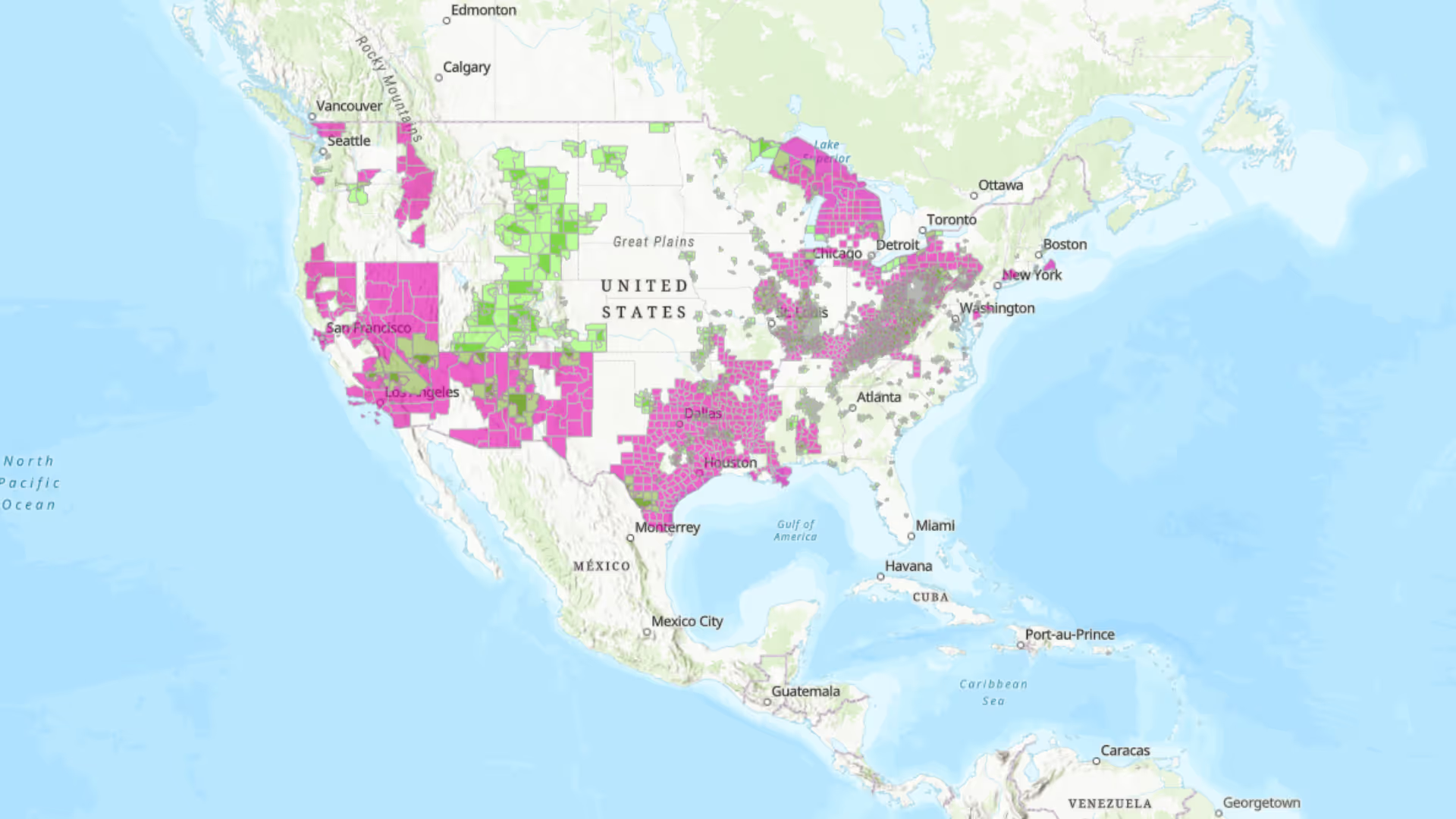

With the DOE's own energy community map still lagging behind the latest Treasury guidance, developers need reliable, up-to-date tools to verify project eligibility. That's why we built the Basis 30C/ITC Adder Map — a free, interactive resource designed specifically for clean energy developers who need fast, accurate answers.

What makes the Basis map different:

Whether you're a developer stress-testing a pipeline, a tax equity investor running diligence, or an advisor modeling credit values, the Basis map is built to save you hours of manual lookups.

A couple of other industry resources have also adapted to the new guidance:

Understanding when your project needs to qualify as being in an energy community is crucial for securing the bonus credits. The rules differ depending on your tax credit type:

Investment Tax Credits (ITC): Eligibility for the energy community bonus credit is determined on the date that the project is placed in service and is not tested again.

Production Tax Credits (PTC): Projects have more flexibility. If the project owner determines that the project is eligible for the energy community bonus credit on the date construction is considered to have started for tax purposes, then the project will qualify for the bonus credit for the entire ten-year PTC period and is not tested again.

This means a project qualifies if it either:

1. Verify Current Project Locations: Check all active projects against the updated lists to confirm continued eligibility or identify new opportunities.

2. Review Development Pipeline: Projects in counties that shifted between census statistical areas may have gained new qualification paths.

3. Update Financial Models: Because eligibility is determined on a placed-in-service date that is subject to potential delays, developers should think carefully about how to incorporate the statistical area category into their financial assumptions.

Planning Considerations

The annual nature of these updates creates both opportunity and uncertainty. The statistical area category changes every year, based on the prior year's unemployment rate. This means areas can gain or lose energy community status, making timing critical for project development.

However, there's good news for coal closure areas: Unlike the statistical area category, the coal closure category cannot shrink; once an area qualifies as a coal closure, it remains as such for the duration of the energy community bonus.

Looking Ahead

The notice's list of energy communities for the Statistical Area Category is effective from June 23, 2025, until the release of next year's annual update. Based on historical patterns, expect the next update around May 2026.

For coal closure categories, some updates have retroactive effects, so it's worth checking whether any of your past projects might now qualify for credits they previously couldn't claim.

The 2025 energy community map updates offer both new opportunities and require careful attention to timing. With the expanded statistical area criteria and updated coal closure lists, more projects may qualify for valuable tax credit bonuses. However, the annual nature of these changes demands that developers stay vigilant about eligibility status throughout project development.